Razer Bank: SME’s preferred bank

my first hackathon

Summary

![[celebratory] never imagined we would make it and we actually slept through the next evaluation round • linkedin](https://images.squarespace-cdn.com/content/v1/5dcbda70786ea45cda1b2ed9/1590025017912-VUOQF1J1PFGRJ267342A/Header-celebratory.png)

[celebratory] never imagined we would make it and we actually slept through the next evaluation round • linkedin

Razer held a two-day Fintech Digital Hackathon where we had to solve one of five problems. Our solution? A complementary app to help SMEs get (1) more sources of funding easily and (2) have more means of digitalising their business.

[This project is Singapore-specific 🇸🇬]

role

UX Designer: In-charge of usability and translation of business objectives

timeline

(2 days) 15 - 16 May 2020: Idea and Proof of Concept

why this hackathon?

I was introduced to this in a casual chat with an acquaintance and I was interested in knowing what potential problems were needed to be solved in the FinTech sphere. Having personally visited the Razer Fintech booth in the Fintech Festival 2019, I was interested to know and gauge what their potential strategies are to enter the already-saturated market*.

*Consumers are already overwhelmed with the multiple cashless payment options by banks and other tech companies (e.g. GRAB Pay, PayNow, PayLah, FavePay) so what would RazerPay’s USP be?

the team 👩💻

We were a team of four fresh graduates:

Yuan Qi, our' ‘senior consultant #1’ 👩💼– She has previously done finance and accountancy-related case competitions and has done stints related to consumer banking.

Benedict, our ‘senior consultant #2’ 👨💼– He has a background in Finance and has done stints related to investment banking.

Marlene, our developer 👩💻– She has a Computer Science background and does UX, front-end and back-end coding. #blessed

Guo Kang, our ‘ghost consultant’ 👻– Fam had a passion, sadly, he wasn’t qualified to participate for he wasn’t a citizen or a permanent resident yet, he was interested in the challenge. He has a background in Finance and Product!

Apart from Marlene, this was our first hackathon and honestly didn’t know what to expect. Even so for her, this is the first FinTech hackathon that seems to require an equal weightage of strategy and development which was uncharted waters for all.

where do i come in?

what’s missing?

we have the “Business Perspective” and the “Technical Perspective”.

In comparison, my niché is in Marketing (which seems out of place here). However, during the hackathon, my role was to:

Bridge the understanding and requirements between the '“senior consultants” (‘Yuan Qi’ and ‘Benedict’) and our developer (‘Marlene’) – I don’t have as much finance knowledge compared to my peers but I am able to simplify and provide context to the developer when coding

Translate into user-friendly content – Our solution was a washed-down, lite version of the investment platform out in the market (i.e. CapBridge, Validus) so must be able to distill what’s crucial.

okay, let’s dive right in…

Provided with five broad questions, our team honestly took one day to deciding which to work on, weighing it’s pros and cons. We decided to work on the following:

Digitalization strategies are not apparent to SMEs*; with significant frustration on difficulties in accessing grants & support schemes

“Put yourselves in the shoes of your startup or SME: create holistic fundraising support tools for quick and efficient access to vital capital.”

SMEs* or Small-Middle Enterprises can also be referred to as start-ups

simply put,

this problem comes in two parts we have to address:

Digitalization Strategies 🖥️

Accessing Funds 💵

PART 1: digitalization strategies 🖥️

Singapore is a very small country and for SMEs to compete regionally and globally, it’s to their advantage to move digital.

“Digital transformation increases a firm’s value by ~25% and productivity by ~16%”

PART 2: accessing funds 💵

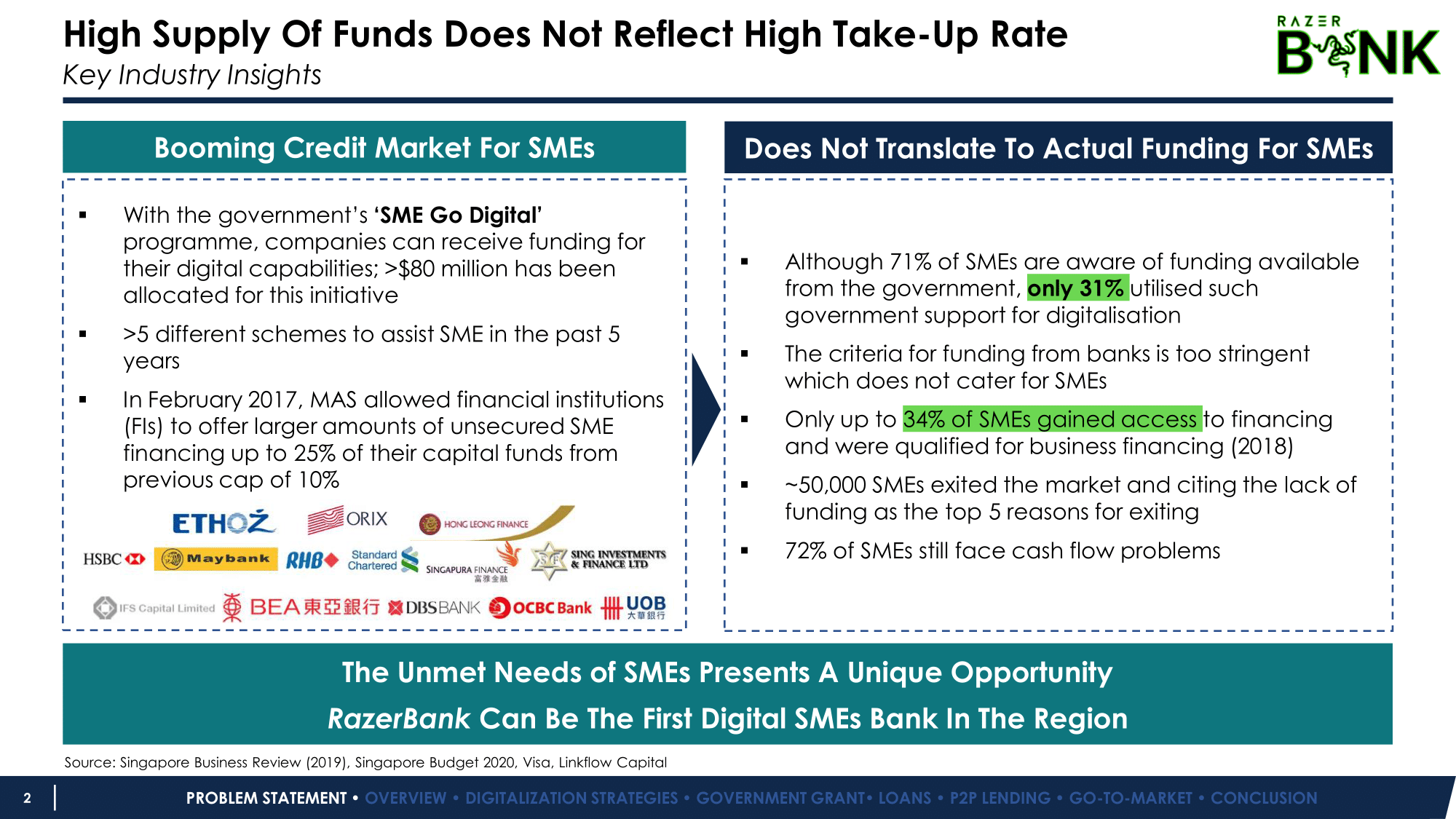

There is a booming credit market for SMEs, meaning there’s many opportunities of funding, such as (A) Government Grants and (B) Loans.

However, only 31% of SMEs utilise such government support for digitalisation. On top of that, traditional cookie-cutter loan requirements* discriminates against SMEs.

*Requirements include:

Collateral 📝🔒– 1 in 4 SMEs are unable to produce required collateral to qualify for a loan

Revenue 💵– Minimum annual revenue of $300k / year is required BUT SMEs may not meet this requirement

Operational History 📊– Most banks require a minimum 2 to 3 years of operating history BUT most of the time, new start-ups requires funds more urgently

Cashflow 💵🔁– Banks require stable cash flow with minimal fluctuations (but we all know, it’s hard for start-ups)

Good Credit Rating 🏅– Company directors are required to provide personal guarantees

“~50,000 SMEs exited the market and cited the lack of funding as the top 5 reasons for exiting”

sketch of the solution when planning

introducing, Razer Bank: Your Preferred SME Bank

Razer will function as a bank 🏦 for SMEs, with transactions all dealt with via RazerPay. We initially intended for the platform to be done via Web, however, after taking a look at what’s available in the market, we realised that there’s A LOT of information 📰 to be provided by both SMEs and Investors.

HENCE, for this hackathon, we focused on creating a complementary phone app.

Document upload will still happen mostly via Web. Platforms in the market are already standardised.

Hence we only work on creating a phone app that is complementary and value-adding. (Screenshot taken from Validus)

complementary phone app 📲

Needless to say, the behaviour for a phone app will be different from a web platform. We envisioned for the phone app to be for activities on the lighter side of things, such as:

Checking on application status – for grants, loans, etc.

Checking on relevant information – for light reading, possibly during commute or meal times

With that, we excluded the flow of uploading important documents because that’s with the assumption it will be handled during account set-up on Web.

overview of key features

The following are the key features 🔑 of the complementary app:

E-Wallet 👛 to monitor all funding & transactions

Easy Apply 👆 for Grants & Loans (ft. Syndicated Loans)

P2P Lending (ft. Chat Function 💬 !)

Gamified 🎮 checklist to Digitalise the Business

More will be explained below

from a monetization perspective 💰,

compared to competitors in the market, this is something that has yet to be done. When comparing each category, we will be more attractive 🤑 in the following:

Payment Network – Transaction fee (lower than benchmark)

Loans – Introduction of syndicated loans (which is usually only used for huge amount)

P2P Lending – Subscription listing fee, success fee basis, and commission on interest payment

Grants – No fees when utilising search algorithm!

GO-TO-MARKET SLIDE • TAKEN FROM PITCH DECK

Before SMEs can access this app,

they first have to update basic details on the company, such as the industry their company is in, when were they established, etc via the web version 🖥️. From there, we are then able to get an understanding of how we should tailor our content 🧵 for them subsequently.

#1: e-wallet 👛 to monitor all funding & transactions

This app will allow SMEs to have an overview of the balance of their finances, along with the status success of their fundraising. It also gives them an overview as to where the funding is coming from, and the status of their loan application.

integrate razerpay

Additionally, this provides a good opportunity for Razer to integrate their RazerPay system, which can be linked to the SMEs’ various bank accounts. It will function as a centralised digital payment system.

Loans and grants would be disbursed from RazerPay directly, and repayments will be deducted from SMEs’ balance.

razer credit scoring system

With prolonged usage of Razer Bank, a Razer Credit Scoring will be calculated, and this score will be utilised as one of the scoring assessment tools when the SME applies for a loan.

The credit scoring factors the SME’s payment history between creditor and suppliers, cash balances of account and spending behaviour.

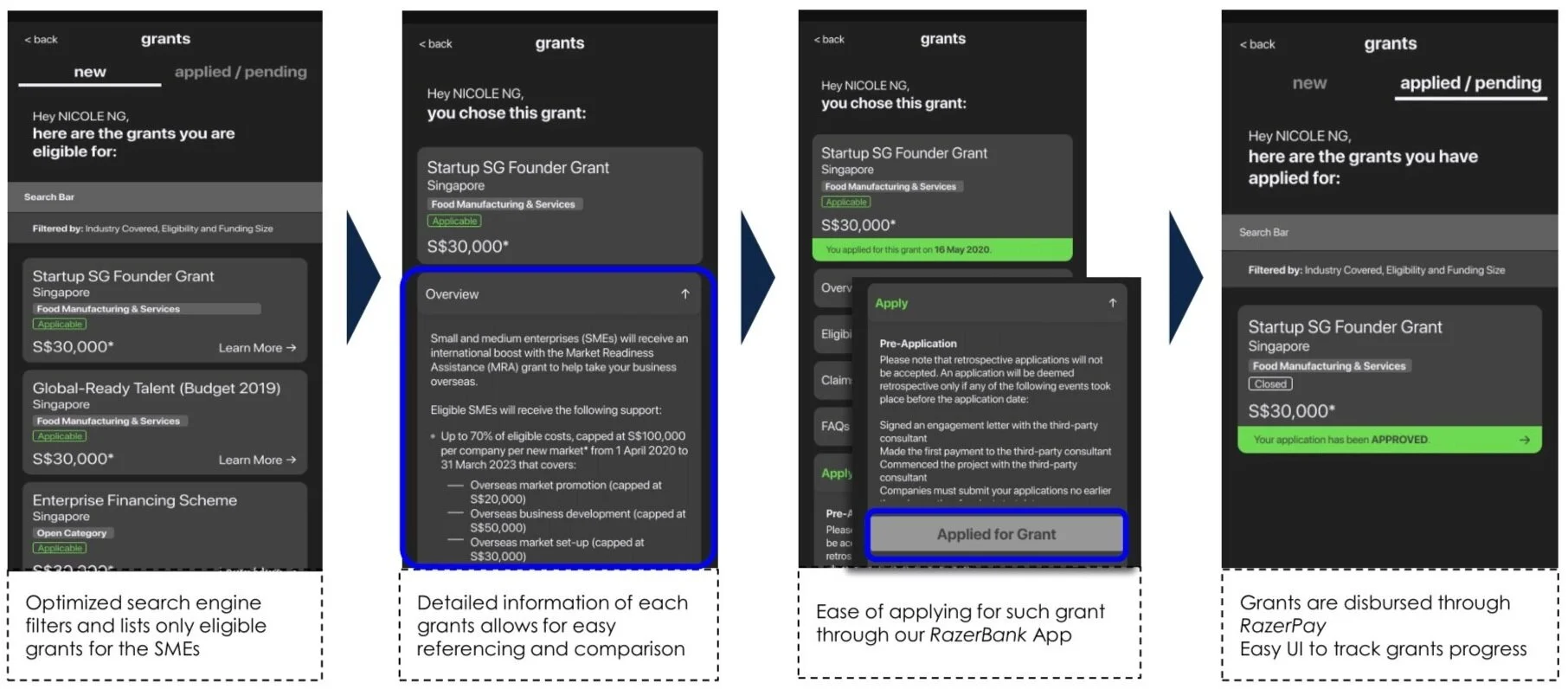

#2: easy apply 👆 for grants & loans (ft. syndicated loans)

think: LinkedIn “Easy Apply” function

Just one click!

As mentioned earlier, there’s no one consolidated stop for SMEs to monitor their funding and applications and thus, the “easy apply”!

grants

For grants, this is something that definitely can be done by Enterprise SG as an extension of their current platform.

grant • taken from pitch deck

loans

For loans, how it works is that the SME will submit their loan proposal to Razer Bank, who would then send to banks on their behalf and compare all the bank loans for their comparison. Since there’s a form of comparison, “syndicated loans” can be introduced.

Syndicated loans have generally been used for huge amounts but this also lessens the burden on the banks should they not want to loan out so much.

LOANS • taken from pitch deck

Traditionally, SMEs have to send each and every application to the banks themselves and rarely do they have the opportunity to compare the rates at a glance.

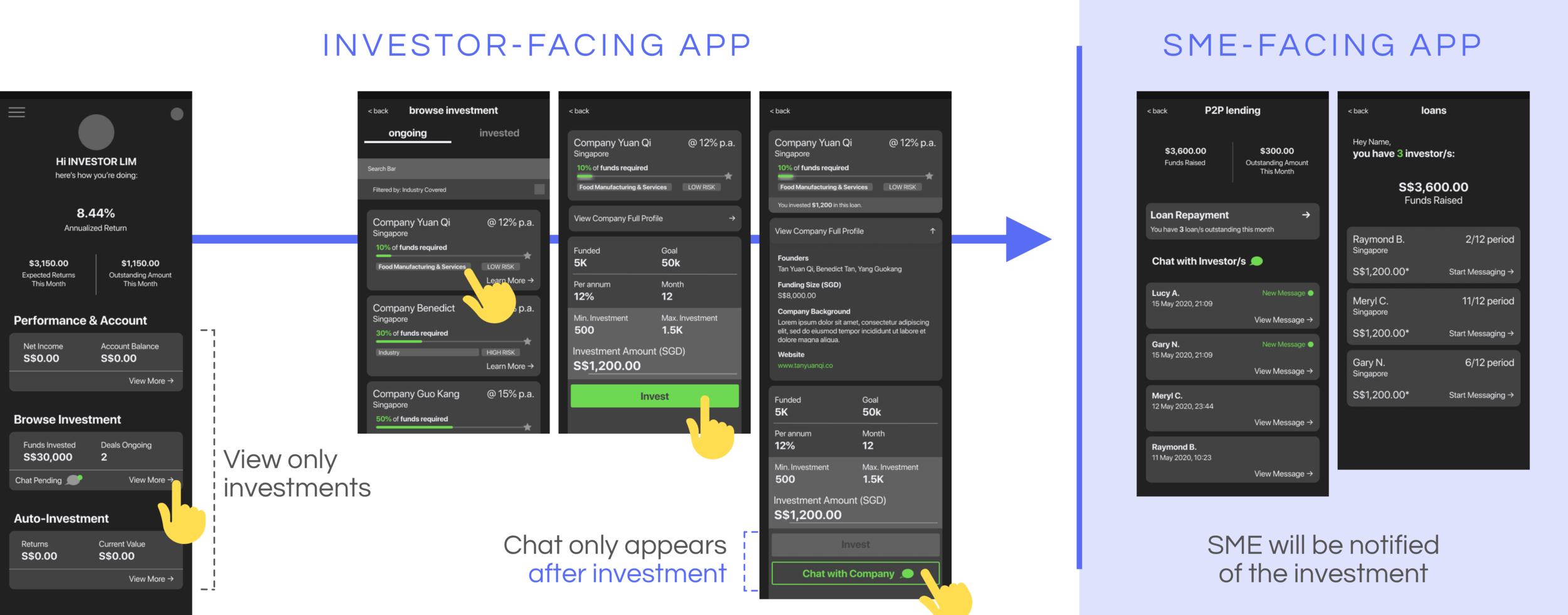

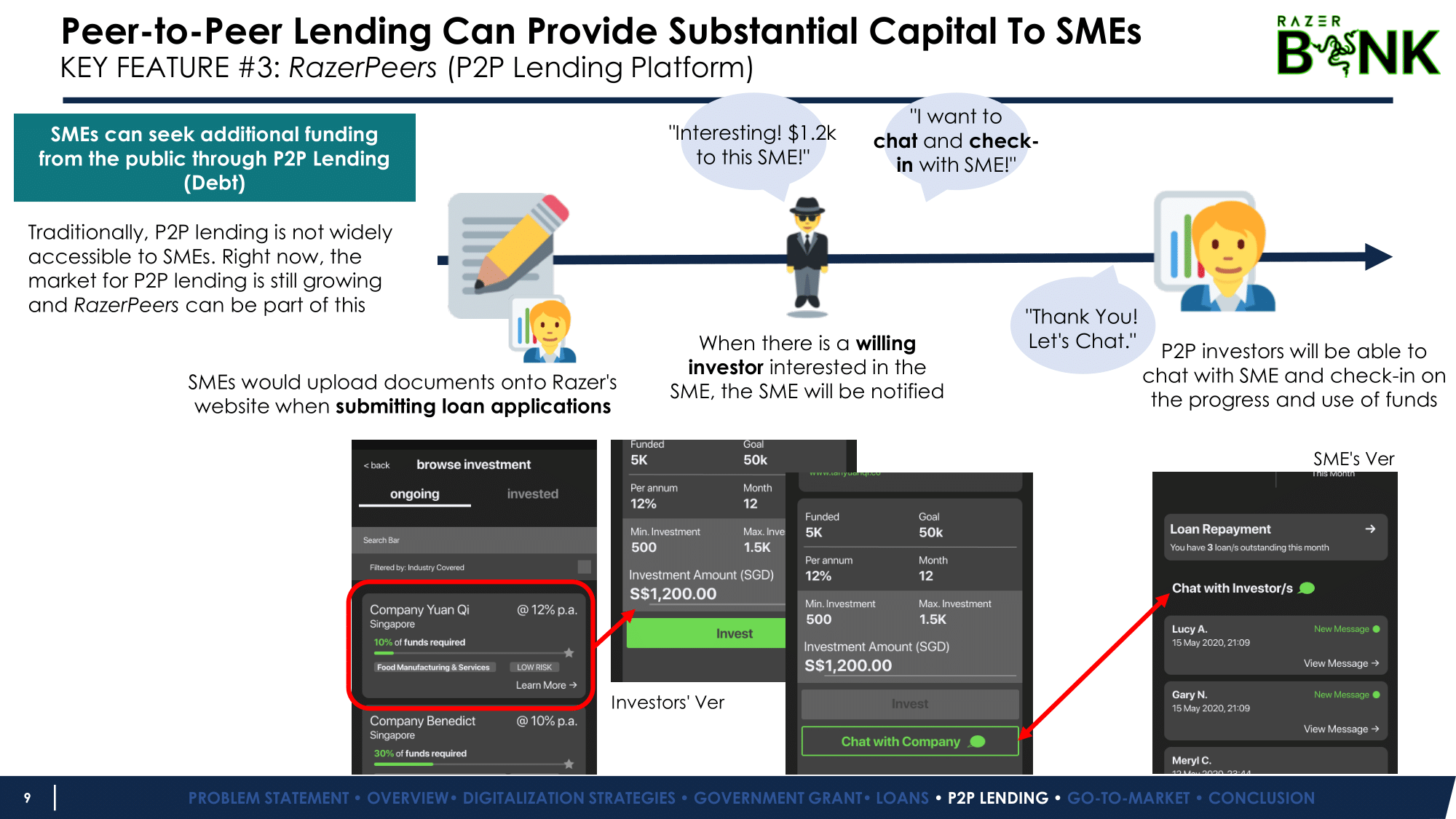

#3: P2P Lending (ft. chat function 💬 !)

Currently, in the market, P2P Lending does exist (See: Funding Societies). However, the chat function does not exist and this is something that can be brought in. For the prototype, we created an investor-facing app along with the SME-facing app.

We see the potential for investors to just check-in on the SME if there’s any doubts, however, we are only allowing the chat function to be provided AFTER the investment. Currently, P2P Lending is preferred due to its fast and simple transaction, hence, chat function is introduced afterwards.

#4: gamified 🎮 checklist to digitalise the business

Based on SME Portal, we have streamlined possible aspects of digitalization to 12 modules. When clicking into it, Razer Bank would feature the “best-in-class” practices and outcome of the SME’s industry. This is to provide greater context and relevance as to why it’s crucial to digitalize that aspect of their business.

To complete the module, the SME has to purchase a relevant software through RazerPay. Should the SME already have a similar software purchased, they can upload proof of purchase to claim.

Should the SME finish any 4 modules, they are able to get an incentive: which we set it for 20% discount off Razer laptops (or any product that would be beneficial for the business).

caveat

We provided a 8C4 (8 Choose 4) situation because we understand that not all aspects of digitalization would be useful to a business. We also understand that each module has overlaps and is very difficult to ascertain whether or not a business has indeed digitalized.

How many firms in the market are doing, such as OCBC Business Dashboard, is that they link SMEs to IMDA and Enterprise Singapore’s consultants to ensure they can work towards obtaining a loan.

placement of information 📐

purpose to user 👨💼👌

This is apparent in the ‘Home’ section for both investors’ and SMEs. We aim to only show what is relevant.

sensitive information like the details of funds transactions should be hidden.

easier for dev efforts 👩💻👍

Having used up 26 hours to decide on the strategy, this means we only have 24 hours to conceptualise the design and have it coded. Thus, Marlene and I worked on modularizing the app 🧱 and utilising repeated elements such that it’s easier to develop.

EXAMPLE, THE INFORMATION PRESENTED (LAYOUT) IS THE SAME FOR LOANS, P2P LENDING AND GRANTS.

colour scheme used 🎨

It was my first time experimenting with colours for Dark Mode, (especially with Razer’s brand colour that screams “Stealth!” and “Mystery”), it’s honestly a crime not to go dark. Having an immense crash course from Material Design, various colours were experimented with, till it came to a critical question:

WHAT IS THE FEELING WE WANT TO CONVEY?

On one hand, utilising Razer’s brand colour no doubt makes it a much stronger branding, leveraging on its global presence. However, it’s known worldwide as a gaming company. Would a user trust it’s finances to a gaming company? Maybe not.

On the other hand, utilising other cool and warm shades of dark mode provides a sense of security, due to what’s already in the market, such as Funding Societies.

colour experimentation

which provides the feeling we want?

All in all, it was a fun (and definitely tiring 😪) experience but it was a learning point for us all. Many business students have gone through case competitions, thinking of strategies. However, most are not exposed to hackathons and therefore, how to translate it into actual products.

Found below is the 10-page slide deck which we submitted, along with the prototypes to play around with:

click to go to android emulator

click to go to github

click to go to ios simulator